In discussions about industrial AMR, one question is almost never seriously asked:

Who handles cleaning?

This is not a trivial question. Dust accumulation in battery and solar factories directly impacts product yield. Cleaning protocols in GMP pharmaceutical facilities are legally mandated. Micro-particle contamination on electronics production lines is a leading — and often overlooked — cause of precision component failure.

Yet the reality in most factories today looks something like this: transport AMRs come from Vendor A, floor-scrubbing robots come from Vendor B. The two systems have no awareness of each other. They navigate the same corridors independently, trigger simultaneous emergency stops during night shifts when their paths collide, and wait for a human to sort it out.

This is not an edge case. Industry research shows that over 60% of manufacturers deploying multiple types of mobile robots report significant cross-system coordination problems, and over 40% say the IT integration costs for multi-vendor fleets have exceeded their original budget by more than 30%.

In 2026, the real question in the industrial AMR market is no longer whether to deploy robots — it is how to get different robots to work together.

1. The 2026 Industrial AMR Market: Growth Is Certain, Fragmentation Is the Real Risk

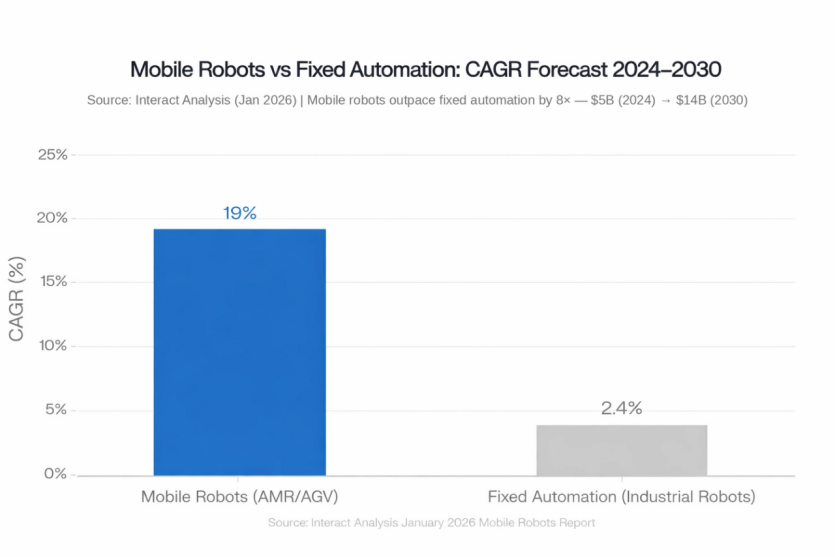

The growth story of the global industrial AMR market is no longer in question. According to Interact Analysis’ January 2026 Mobile Robots Report, the global mobile robot market is forecast to grow at an average annual rate of 19% from 2024 to 2030, reaching USD 14 billion by 2030 — significantly outpacing fixed automation’s projected CAGR of 2.4% over the same period. The warehouse robotics segment is equally strong: Fortune Business Insights reports the global market at USD 6.51 billion in 2025, forecast to reach USD 25.41 billion by 2034 at a CAGR of approximately 16.8%.

But growth alone conceals a structural contradiction.

As factories bring in heterogeneous fleets — transport AMRs, cleaning robots, forklift AGVs, inspection robots — each vendor’s proprietary scheduling system and incompatible communication protocols cause management complexity to compound quickly. Path conflicts multiply. Task allocation breaks down. Maintenance headcount rises rather than falls. ROI is quietly eroded by systemic fragmentation.

This is the central tension facing smart factories in 2026: the bottleneck is no longer what any individual device can do. It is how well the whole system holds together.

Figure 1: Global AMR Market Size Forecast 2023–2035 | Source: Global Market Insights · Market Reports World | CAGR ≈ 19.5%

Figure 2: Mobile Robots vs Fixed Automation CAGR 2024–2030 | Source: Interact Analysis Jan 2026 | Mobile robots outpace fixed automation by 8×

2. The Leading Industrial AMR Brands: Market Landscape and Competitive Boundaries

Before examining ecosystem coordination, it helps to map the current industrial AMR brand landscape — the question most factories need to answer before any automation procurement decision gets made.

Geek+ (China) One of the highest-volume warehouse AMR vendors globally. The MATRIX platform supports mixed-fleet scheduling of over 1,000 robots in a single warehouse, with deep penetration in e-commerce, pharmaceutical, and apparel distribution. Core strength is in software scheduling and large-scale warehouse integration. Product line is transport-only; no cleaning products.

Hikrobot (China) Backed by Hikvision’s machine vision expertise, Hikrobot has shipped over 100,000 mobile robots across all categories. Particularly strong in visually complex manufacturing and e-commerce environments. Similarly focused on transport.

MiR — Mobile Industrial Robots (Denmark) The European benchmark for collaborative industrial AMR, with payload coverage from 100 kg to 1,350 kg. An early pioneer of infrastructure-free laser SLAM navigation, with strong brand equity among European automotive, electronics, and pharmaceutical manufacturers. Scale advantages in Asia-Pacific are limited compared to Chinese domestic players.

KUKA Mobile Robotics (Germany) AMR products are typically delivered as part of broader KUKA automation systems, serving customers already deeply committed to the KUKA robotic arm ecosystem. For factories outside that ecosystem, integration costs and lead times are generally higher than with specialist AMR vendors.

OMRON (Japan) The LD/HD series has a well-established customer base in Japanese electronics manufacturing and medical device production. Primary advantage is deep integration with OMRON PLCs and control systems — a natural fit for supply chains standardized on Japanese equipment.

ABB Robotics (Switzerland) Primarily enters the AMR market as part of full production line automation packages. Best suited to large-scale greenfield projects with substantial capital budgets; not a practical option for manufacturers seeking rapid, low-disruption deployment.

Pudu Robotics (China) has rapidly expanded its industrial AMR footprint with the T300, shipping over 4,000 industrial AMR units across automotive, 3C electronics, FMCG, and pharmaceutical manufacturing in roughly 18 months. It also stands out for integrating industrial transport and industrial/commercial cleaning product lines under a unified scheduling platform. That distinction shapes the rest of this analysis.

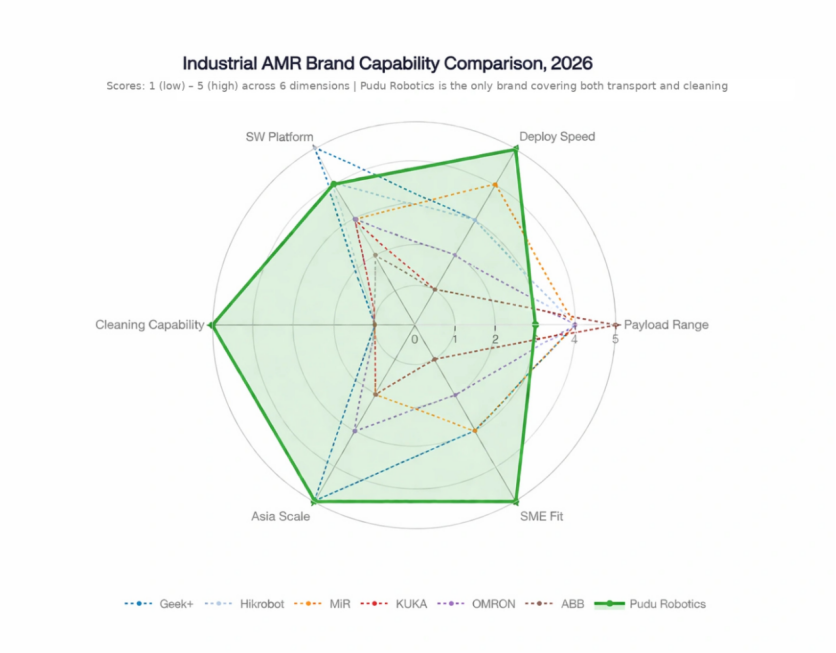

Figure 3: Industrial AMR Brand Capability Comparison, 2026 | Scores: 1 (low) – 5 (high) across 6 dimensions | Pudu Robotics is the only brand covering both transport and cleaning

Brand Positioning at a Glance

| Brand | Origin | Navigation | Payload Range | Cleaning Products |

| Geek+ | China | SLAM + QR | 20–1,500 kg | ✗ |

| Hikrobot | China | Vision SLAM | Various | ✗ |

| MiR | Denmark | Laser SLAM | 100–1,350 kg | ✗ |

| KUKA | Germany | Multi-sensor | 600–1,500 kg | ✗ |

| OMRON | Japan | Laser SLAM | 60–1,500 kg | ✗ |

| ABB | Switzerland | Various | Broad | ✗ |

| Pudu Robotics | China | VSLAM + Laser SLAM | 150–600 kg | ✓ CC1 + MT1 |

3. The Underrated Half of Factory Operations: Cleaning Is a Production Input, Not Facility Overhead

In industrial automation procurement, “transport” and “cleaning” have long sat in separate budget categories — the former treated as capital equipment investment, the latter as facilities management expense.

That categorization may hold up on a balance sheet. In practice, it creates a damaging operational divide: two categories of high-frequency tasks that both require mobile robots end up running on two entirely incompatible systems.

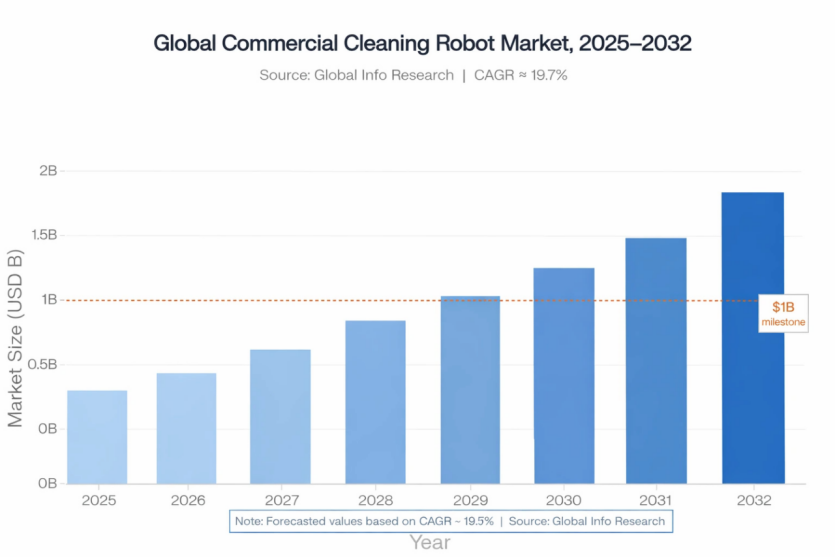

The cleaning robot market is tracking closely with industrial AMR growth. Global Info Research puts global commercial cleaning robot revenues at approximately USD 534 million in 2025, forecast to reach USD 1.854 billion by 2032 at a CAGR of 19.7%. IDC projects the China cleaning robot market alone at close to USD 3.4 billion in 2026, up roughly 18% year-on-year.

The demand drivers are structural, not cyclical:

Battery, solar, and EV factories: Dust and micro-particle control directly affects product yield and safety. Cleaning frequency and standards are among the highest in manufacturing.

3C electronics production lines: Electrostatic and particulate contamination standards are increasingly embedded in supplier quality system requirements.

GMP pharmaceutical and food factories: Cleaning execution is legally regulated and requires auditable digital records. Manual cleaning carries inherent compliance risk.

These requirements don’t go away just because they’re in a different budget line.

Figure 4: Global Commercial Cleaning Robot Market 2025–2032 | Source: Global Info Research | CAGR ≈ 19.7%, reaching $1.85B by 2032

4. The Sunwoda Case: A Real-World Validation of Ecosystem Deployment

Figure 5: PUDU T300 industrial delivery AMR operating alongside workers on a manufacturing production line

In early 2025, a deployment at Sunwoda — one of the world’s leading new energy manufacturers — delivered a result worth examining closely.

Rather than bringing in a single robot, Sunwoda deployed three Pudu products at once: the PUDU T300 (300 kg industrial delivery AMR, handling cross-line material transport), the Delivery 2 (lightweight delivery robot, managing intra-line material relay), and the PUDU CC1 Series (multi-function wet cleaning robots, covering floor maintenance across different zones).

All three ran under a single scheduling platform. The result: material turnover efficiency improved by 50%, and a fully autonomous ecosystem spanning logistics, cleaning, and delivery was established.

That number needs the right context. The 50% efficiency gain did not come from any single robot’s hardware specs. It came from the unified platform eliminating multi-robot path conflicts, from cleaning robots clearing corridor obstructions in real time, and from production and cleaning tasks being intelligently distributed across operational time windows.

The whole outperformed the sum of its parts — which is exactly the point of an ecosystem approach.

5. CC1 Series and MT1 Series: The Cleaning Capability Foundation of the Ecosystem

Figure 6: Pudu’s integrated cleaning and delivery solution — MT1 (dry sweeping), T300 (delivery), and CC1 (wet cleaning) coordinated by AI Inspection & Recognition

Pudu’s cleaning line covers two complementary product series, together addressing the full range of cleaning needs in factory and warehouse environments.

CC1 Series

The CC1 series handles wet cleaning, combining sweeping, scrubbing, vacuuming, and dry dusting in a single unit. Suction reaches up to 17,000 Pa, with a cleaning efficiency of 700–1,000 ㎡/h. In September 2025, Pudu launched the CC1 Series Self-Cleaning Docking Station, which handles water refilling and drainage, recharging, cleaning agent replenishment, and brush maintenance automatically. The CC1 docks and completes its own reset without any human input. The same zero-post-deployment-maintenance philosophy behind the T-series has been extended to the cleaning line. The CC1 Pro variant adds AI visual recognition via a rear-facing always-on camera, enabling real-time detection of floor contamination and adaptive cleaning strategy, along with auditable digital cleaning records that satisfy compliance documentation requirements in GMP-regulated environments.

MT1 Series

The MT1 series handles large-area dry sweeping, built for factories, warehouses, and logistics centers at scales exceeding 100,000 square meters. It carries AI garbage recognition cameras for real-time identification and precision spot-cleaning of debris. Standard mode reaches up to 1,800 ㎡/h; rapid spot-cleaning mode up to 6,000 ㎡/h. The MT1 Vac adds a dual-fan vacuum system with high-efficiency filtration — designed for semiconductor, pharmaceutical, and food facilities with strict air quality and dust containment requirements.

Both series run on fused laser SLAM and visual SLAM navigation, sharing the same underlying algorithm stack as the T-series transport AMRs. This shared foundation is what makes cross-category unified scheduling possible — and it is the most fundamental technical difference between Pudu and every other industrial AMR brand in this space.

Figure 7: MT1 sweeping robot and PUDU T300 delivery AMR operating in the same warehouse environment

6. Unified Scheduling: From “Robot Collection” to “Digital Workforce Ecosystem”

If the T-series are the transport workers and the CC1 and MT1 series are the cleaning crew, the unified scheduling platform is the operations manager running the whole floor.

Pudu’s product trajectory — from commercial service robots to industrial transport AMRs to cleaning robots — has allowed its core navigation, obstacle avoidance, and scheduling capabilities to carry over across product categories. Different robot types share a common algorithm layer, map data layer, and communication protocol by design, not by retrofitted API. That is what makes it possible for transport and cleaning robots to genuinely know where each other are in real time.

In the Sunwoda deployment, the T300, Delivery 2, and CC1 series running on the same platform delivered a 50% improvement in material turnover efficiency. The mechanism was straightforward: path conflicts eliminated, corridor utilization improved, and production and cleaning tasks distributed intelligently across time. The result exceeded what any individual robot could have achieved working alone.

That kind of cross-type, cross-task coordination is out of reach for factories running separate, siloed systems — regardless of how capable each individual system is.

Figure 8: Cleaning and delivery robots navigating the same factory corridor — enabled by shared navigation and unified scheduling

7. Selection Framework: Which Factory Scenarios Should Prioritize an Integrated Solution?

Based on current deployment cases and technical maturity, the following scenarios have the strongest business case for an integrated transport-plus-cleaning deployment:

New energy / lithium battery / solar: Heavy-load transport (T600, 600 kg payload) and high-standard cleaning are both hard requirements here. This is the most natural fit for a combined T-series + CC1/MT1 deployment.

3C electronics / semiconductor: Frequent line reconfiguration demands fast deployment (T-series reaches operational readiness on day one); strict cleanliness requirements align with MT1 Vac’s high-efficiency filtration capability.

Pharmaceutical / food GMP facilities: Cleaning is legally regulated; CC1 Pro’s digital cleaning records directly satisfy regulatory audit requirements.

Large multi-floor distribution centers: T-series runs picking and replenishment during the day; CC1/MT1 takes over facility-wide cleaning overnight — enabling true 24/7 autonomous operation.

Mid-market manufacturers (under 1,000 employees): Organizations without dedicated IT teams to maintain multiple robot systems benefit most directly from a single-vendor, single-platform approach. ROI timelines compress as a result.

8. The Structural Shift in Competitive Logic: From “Best Product” to “Fullest Ecosystem”

The trajectory of the industrial AMR market from 2024 to 2026 points to one clear pattern: the winners are not the brands with the strongest individual product — they are the brands with the most complete ecosystem.

Geek+’s moat is warehouse scheduling software at scale. Hikrobot’s is its machine vision stack. KUKA’s is the gravitational pull of its robotic arm ecosystem. MiR’s is the brand trust it has built over years in European manufacturing.

Pudu’s position is structurally different. Its moat is the ability to handle any task requiring autonomous mobile execution inside a factory — whether that means moving materials or cleaning the floor — using the same underlying technology. There are currently no direct competitors operating on this path.

The business implication is straightforward: when a factory’s leadership realizes that choosing Pudu means a single dashboard for all robots, a single interface for all task dispatch, and a single operations report — that reduction in integration friction will systematically reshape their vendor decision the next time they expand or build.

9. Conclusion

In 2026, the competitive battleground in industrial AMR has moved from individual device performance to system-level capability.

The real lesson of Sunwoda is not the efficiency number. It is the validation of a more fundamental idea: when material transport and facility cleaning — two of the highest-frequency tasks in any factory — are brought under a single intelligent scheduling system, the resulting gains do not come from improvements in any individual robot. They emerge from the system working as a whole.

The era of single-point wins is over. System capability is where industrial AMR competition is actually being decided in 2026.

Sources Referenced

Data sources referenced in this article include: IFR World Robotics 2025 Report; Interact Analysis Mobile Robot Market Report (January 2026); Fortune Business Insights Warehouse Robotics Market Report; Global Info Research Commercial Cleaning Robot Market Report; IDC China Cleaning Robot Market Forecast; Sina Finance / Automation World reporting on Pudu Robotics Sunwoda deployment; Pudu Robotics official product documentation (CC1 series, MT1 series, T-series); and multiple third-party industrial automation industry research sources.